Driving defensively is something that students learn when they first take the wheel. You have to not only pay attention to your own driving, you have to anticipate the actions of other drivers and plan accordingly, giving yourself enough time and distance to react properly.

The same holds true when it comes to purchasing auto insurance. Many motorists think they’re adequately covered if they have insurance that protects them in the event that they’re at fault in an accident. But if you really want to protect yourself and your assets from an economic crash, you have to anticipate the crazy things others on the road might do — like driving without any insurance at all. That’s why uninsured motorist coverage is a smart investment.

WHAT IS UNINSURED MOTORIST COVERAGE?

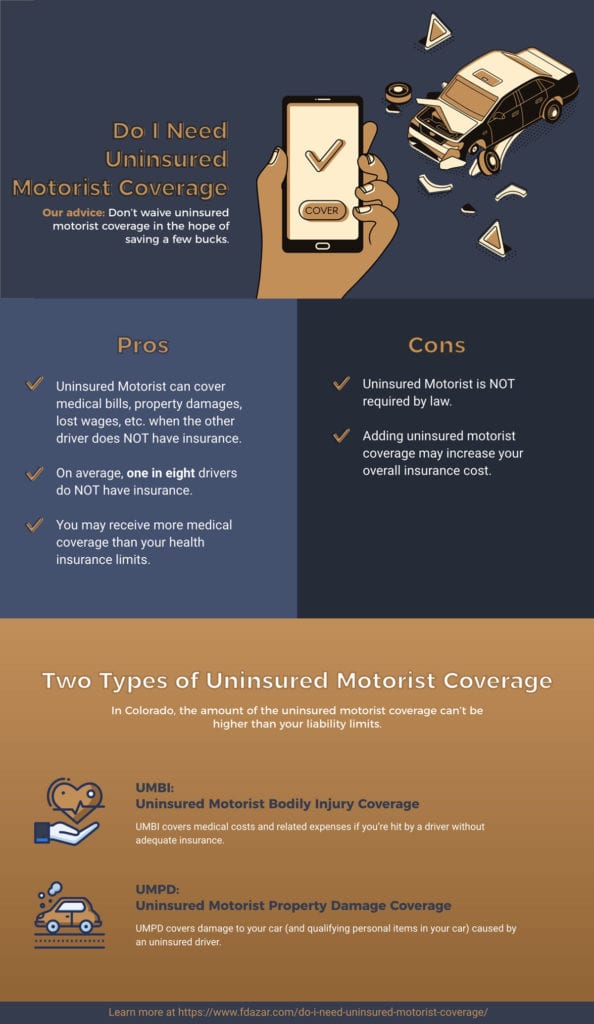

Uninsured motorist coverage covers your losses from being hit by a driver who does not have insurance.

State laws require all drivers to carry insurance on their vehicles. But the Insurance Research Council estimates that as many as one in eight drivers on the road is driving without insurance. Arranging for uninsured motorist coverage in your own insurance package protects you from not being able to recover the losses resulting from a crash caused by an uninsured driver. It also helps to make up the difference if the at-fault driver is under insured, meaning the costs arising from the accident exceed that driver’s liability coverage.

TWO TYPES OF UNINSURED MOTORIST COVERAGE: UMBI and UMPD

There are two basic types of uninsured motorist coverage, one for bodily injury coverage (known as UMBI), which covers medical costs and related expenses if you’re hit by a driver without adequate insurance, and one for property damage (UMPD).

In Colorado, insurance companies are required to offer UMBI as part of any standard auto policy, unless you formally waive that coverage in writing. You can also purchase additional UMPD insurance to cover damage to your car caused by an uninsured driver, but depending on the policy and deductibles involved, that damage may also be addressed through collision and comprehensive coverage.

Whatever you choose, the importance of the uninsured/underinsured coverage for bodily injury can’t be stressed enough. The coverage doesn’t just give you peace of mind behind the wheel; it also can cover your medical expenses if you happen to be injured as a pedestrian (or while operating a bike or electric scooter) by an at-fault, uninsured driver.

HOW MUCH UNINSURED MOTORIST COVERAGE DO I NEED?

In Colorado, the amount of the uninsured motorist coverage can’t be higher than your liability limits.

The minimum liability coverage required by law amounts to $25,000 per person for bodily injury, with a maximum of $50,000 per incident, and another $15,000 in coverage for property damage.

But since medical costs and even just vehicle damage for a higher-end model can easily exceed these totals, it makes sense to sign up for what’s known as 100/300/100 coverage — $100,000 bodily injury coverage, $300,000 per accident, $100,000 property damage.

Drivers with substantial assets to protect might choose to boost the bodily injury limit even higher, covering the bases both for their own liability and in the event of a crash with an uninsured motorist.

One other point: Your insurance agent may tell you that carrying uninsured motorist coverage on one car will “carry over” to other vehicles on the same policy. But that feature doesn’t extend coverage to other passengers that aren’t named on your policy.

If you have teens at home who often transport their friends, or a significant other who’s not listed on your policy, it may be worth it to carry uninsured motorist coverage on all your vehicles.

WHAT DOES IT COST?

A lot less than you might expect.

One 2016 report that analyzed auto insurance costs in several states found that uninsured/under insured motorist coverage (for both bodily injury and property damage) added only between three and nine dollars a month to the cost of the insurance policy. While that might still seem like a burden to those seeking to cut their insurance costs to the bone, there are other ways to reduce your premiums without skimping on critical coverage—for example, by reducing or eliminating collision or comprehensive coverage on an older vehicle, or foregoing rental reimbursement or other bells and whistles.

Our advice: Don’t waive uninsured motorist coverage in the hope of saving a few bucks. It’s the best protection available from that thirteen percent of the motoring population who’ve declined to carry the necessary protection themselves.

THE CAR ACCIDENT LAWYERS AT FDAZAR

For more than thirty years the car accident attorneys at Franklin D. Azar & Associates have helped thousands of injured people obtain complete and timely compensation for their losses. Our proven track record and expertise have allowed us to grow into the largest personal-injury law firm in Colorado, with offices in Denver, Aurora, Thornton, Fort Collins, Greeley, Grand Junction, Colorado Springs, and Pueblo. If you’ve been injured in a car, truck, or motorcycle accident, you may be entitled to compensation. Please call the attorneys at FDAzar day or night at 800-716-9032 or contact us here for a free consultation and no-obligation evaluation of your case.